Key Findings

- The Highway Trust Fund, created in 1956 to finance the Interstate Highway System and other roads through fuel excise taxes, has depended on general revenue transfers for nearly 20 years.

- The funding shortfall stems from several trends: the gas taxA gas tax is commonly used to describe the variety of taxes levied on gasoline at both the federal and state levels, to provide funds for highway repair and maintenance, as well as for other government infrastructure projects. These taxes are levied in a few ways, including per-gallon excise taxes, excise taxes imposed on wholesalers, and general sales taxes that apply to the purchase of gasoline. has not been adjusted for inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spendin, vehicles have become more fuel-efficient, and electric vehicle adoption has grown. Commercial traffic has also underpaid relative to the wear and tear it imposes on highways.

- Without reform, highway spending will exceed highway revenue by $17 billion in 2026. The next five-year reauthorization of highway funding, due in September 2026, offers an opportunity to correct the funding imbalance.

- Restoring the user-pays principle would make highway funding fiscally responsible and economically efficient.

- We present four reform options that could close the 2026 funding gap and move toward a user-based structure. The ideal reform would be replacing existing transportation taxes with a vehicle miles traveled (VMT) taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. that adjusts by vehicle weight per axle, but short of that, several transitional options could strengthen funding and move closer toward the user-pays principle.

- Examples from other countries and US states show that well-designed user fees can fund transportation infrastructure effectively.

Introduction

Current highway authorization is scheduled to expire on September 30, 2026.[1] The legislative process for reauthorization is an opportunity to address structural problems with transportation funding and revenue collection.

For almost 20 years, highway expenditures have exceeded Highway Trust Fund (HTF) revenue, which consists mainly of federal excise taxes on motor fuels—18.4 cents per gallon of gasoline and 24.4 cents per gallon of diesel.[2] Initially, the discrepancy between revenue and expenditures could be blamed on a quirk of the HTF. A small portion of revenue generated from taxes on highway users is reallocated to support mass transit projects under the auspices of the HTF’s Mass Transit Account. But in recent years, total revenue collections to the HTF, including the revenue diverted to mass transit, have not even matched the spending dedicated to highways. The Congressional Budget Office (CBO) projects the HTF will collect $44.2 billion in highway revenue in 2026, while it will spend $61.4 billion—leaving a $17.2 billion gap.[3]

The most recent highway funding authorization, enacted in 2021 through the Infrastructure Investment and Jobs Act (IIJA, or the Bipartisan Infrastructure Law), made no effort to raise additional highway revenue.[4] Instead, IIJA relied on general fund transfers for its new highway spending. The next reauthorization should take a more fiscally responsible approach.

Why User Fees?

User fees are a form of benefits taxes that link payment to use: the people who benefit from transportation infrastructure are the ones who pay for it.[5] Charging users is a more economically efficient way to finance transportation infrastructure than financing transportation through unrelated taxes, such as the income tax.

If one transportation mode is supported by general revenues while a second is entirely reliant on user fees, then people and cargo will shift to the first mode to avoid directly paying. Under user fees, no such distortion would occur, resulting in neutral treatment across different modes of transportation.

Even accepting the user-pays principle, transportation funding faces two major design challenges: adequate revenue and cost-fee alignment. Taxes and fees on highway users should cover highway spending, and rates should reflect the wear and tear caused by different types of vehicles. People who drive more miles or heavier vehicles impose higher costs and should therefore pay more.

Highway funding in the United States fails on both counts.

First, revenues do not cover costs. The primary fuel taxes have not been adjusted for inflation since 1993, while vehicles have become more fuel-efficient, reducing tax collections per mile driven. Growing adoption of electric vehicles (EVs) has also shrunk the tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates.. Although EVs currently make up a small fraction of total vehicle mileage, their dramatic adoption will accelerate future revenue declines.[6]

Second, taxes are misaligned with costs. Heavy trucks are undercharged relative to the damage they cause, meaning freight travel is underpriced.[7] The implicit subsidy for shipping cargo over roads (supported by transfers from the general fund) instead of freight rail (which is privately owned and operated) contributes to greater congestion and road wear.[8]

Fitting into the Bigger Picture

While the HTF’s shortfall is serious, the nation’s overall fiscal challenges are far greater. The HTF is projected to run a $17 billion shortfall in 2026, compared to the overall government budget deficit of $1.7 trillion.[9]

Addressing the federal government’s fiscal imbalance will require reforms to major entitlement programs and, likely, broad tax increases.[10] Fixing the HTF will not solve the bigger problem, but it is an opportunity for lawmakers to adopt policies that improve efficiency and sustainability in one corner of the budget.

The Solution

The solution to both inadequate user charges and the underpricing of freight traffic is a per-mile fee that scales with the amount of damage a vehicle imposes on roads. Such policies are known as road user charges (RUCs), road user fees (RUFs), highway user fees (HUFs), or vehicle miles traveled (VMT) taxes or fees. This paper refers to them collectively as VMT taxes or VMT fees.

Engineering studies consistently show that larger vehicles impose more damage disproportionate to their weight (or more specifically, weight per axle). The precise differences between large trucks and standard vehicles are less clear. One widely cited study suggested an 80,000-pound truck with five axles imposes roughly 9,600 times more damage per vehicle-mile than a 4,000-pound passenger car with two axles. Other studies find the ratio may be closer to 300-to-1.[11] Even under the more conservative estimates, heavy vehicles should pay a significantly higher tax rate per vehicle-mile.

Oregon offers one of the best domestic examples of a VMT tax for commercial traffic, featuring a detailed schedule of rates that vary by vehicle weight and axle count, including for vehicles above 80,000 pounds of gross vehicle weight.[12] In September 2025, Oregon’s legislature passed a transportation bill that would reform Oregon’s VMT structure, though as of this paper’s writing, it awaits the governor’s signature.[13]

A Note on Revenue Scoring

When modeling the revenue effects of excise taxes, we account for income and payroll taxA payroll tax is a tax paid on the wages and salaries of employees to finance social insurance programs like Social Security, Medicare, and unemployment insurance. Payroll taxes are social insurance taxes that comprise 24.8 percent of combined federal, state, and local government revenue, the second largest source of that combined tax revenue. offsets. An indirect taxAn indirect tax, unlike a direct tax such as the income tax, is a tax collected on a product by the retailer or manufacturer; however, the end consumer of the final product ultimately bears much of the burden through the higher price of a good or service. Sales and value-added taxes (VATs) are two examples of indirect taxes. on sales or miles driven reduces the tax base for income and payroll taxes, thus reducing how much revenue they raise.[14] We estimate the income and payroll tax offset averages around 24 percent across the budget window.

In the context of the HTF, a tax increase that closes the gap between highway spending and revenues flowing into the trust fund will have a smaller effect on the overall budget deficit because of the income and payroll tax offset. For example, a tax increase that resulted in $1 flowing into the trust fund would reduce income and payroll taxes by 24 cents, resulting in 76 cents of overall budget deficit reduction.

For each option, we have presented the gross HTF revenue increase (before applying the offset) and the conventional revenue estimate (after applying the offset). We calibrated the rate schedules for each option to roughly close the HTF’s projected $17 billion gap in 2026. For Options 1 and 4, we also present the total (not just the increase) in HTF revenue raised by category of vehicle traffic in 2026.

Option 1: The Full VMT tax

Our proposed VMT tax fully replaces existing HTF taxes. It charges higher rates to heavier vehicles, better representing the damage they impose, resulting in minimal tax increases on passenger travel while also closing the EV hole.

Over the next decade, the VMT tax would raise $270 billion for the HTF and reduce overall deficits by $206 billion. It would raise enough revenue to fully fund highway outlays in 2026, and due to inflation indexingInflation indexing refers to automatic cost-of-living adjustments built into tax provisions to keep pace with inflation. Absent these adjustments, income taxes are subject to “bracket creep” and stealth increases on taxpayers, while excise taxes are vulnerable to erosion as taxes expressed in nominal dollars, rather than rates, slowly lose value., modestly exceed projected highway outlays later in the budget window.

Table 1. 10-Year Conventional Revenue Estimates of Fully Replacing Existing HTF Taxes with a VMT Tax

Source: Authors’ calculations; EIA Annual Energy Outlook 2025, “Table 41. Light-Duty Vehicle Miles Traveled by Technology Type” and “Table 49. Freight Transportation Energy Use”; Bureau of Transportation Statistics, “Annual Vehicle Distance Traveled in Miles and Related Data by Highway Category and Vehicle Type: 2023”; Oregon Department of Transportation, “Mileage Tax Rates Effective Jan. 1, 2022”; Environmental Protection Agency, “Average Annual Vehicle Miles Traveled by Major Vehicle Category”; Congressional Budget Office, “The Budget and Economic Outlook: 2025 to 2035”; Tax Foundation General Equilibrium Model.

A detailed explanation of the rate schedule appears in the appendix. For vehicles under 26,000 pounds, the tax rate is determined by a formula based on gross vehicle weight rating (GVWR). For vehicles above 26,000 pounds, the rates are based on Oregon’s freight VMT tax system. We also adjust the rates for inflation over the next decade.

To illustrate, Table 2 shows average tax rates for different categories of vehicles in 2026 under our proposed full VMT tax. Vehicles with a GVWR of 5,000 pounds, like a small crossover SUV, would face an average rate of 0.89 cents per mile. The commercial truck rate of 10.4 cents would apply to a truck with a GVWR of between 44,000 and 46,000 pounds. Smaller vehicles within each category would face lower per-mile rates, and larger vehicles would face higher rates.

Table 2. Revenue Collected from Full VMT Tax by Vehicle Category, 2026

Source: Authors’ calculations; EIA Annual Energy Outlook 2025, “Table 41. Light-Duty Vehicle Miles Traveled by Technology Type” and “Table 49. Freight Transportation Energy Use”; Bureau of Transportation Statistics, “Annual Vehicle Distance Traveled in Miles and Related Data by Highway Category and Vehicle Type: 2023”; Oregon Department of Transportation, “Mileage Tax Rates Effective Jan. 1, 2022”; Environmental Protection Agency, “Average Annual Vehicle Miles Traveled by Major Vehicle Category”; Congressional Budget Office, “The Budget and Economic Outlook: 2025 to 2035”; Tax Foundation General Equilibrium Model.

Currently, commercial trucks pay roughly 4 cents per mile in fuel taxes, plus small additional per-mile costs from the excise taxAn excise tax is a tax imposed on a specific good or activity. Excise taxes are commonly levied on cigarettes, alcoholic beverages, soda, gasoline, insurance premiums, amusement activities, and betting, and typically make up a relatively small and volatile portion of state and local and, to a lesser extent, federal tax collections. on truck tires.[15] They also pay sales taxA sales tax is levied on retail sales of goods and services and, ideally, should apply to all final consumption with few exemptions. Many governments exempt goods like groceries; base broadening, such as including groceries, could keep rates lower. A sales tax should exempt business-to-business transactions which, when taxed, cause tax pyramiding. on heavy trucks and trailers and a flat highway use fee.

Under the proposed VMT tax, trucks would pay an average tax of 10.4 cents per mile. That’s a substantial increase compared to the status quo, but it’s conservative relative to the estimated cost of truck travel between 4 and 40 cents per mile depending on vehicle weight rating.[16] Importantly, trucks would no longer face the truck sales tax, the flat highway use fee, the tire excise tax, or the diesel fuel tax under this option.

Passenger cars would see only modest changes. Take the owner of a compact sedan with a GVWR of 3,800 pounds and fuel economy of 35 miles per gallon. If they drive 14,000 miles in a year, they consume 400 gallons of gas and pay about $74 in federal gas tax annually. Under the proposed VMT tax formula, they would pay a rate of0.66 cents per mile, and their annual tax liability would be around $92.

This option would impose minimal burdens on passenger car drivers, particularly those with conventionally powered vehicles. A rate schedule that assumed greater relative damage from heavy trucks could hold passenger cars harmless or even result in a net tax cut.

Option 2: Truck VMT Fee, Flat EV Fee, Higher Gas Tax

The full VMT tax accomplishes several key goals: it properly prices freight traffic, eliminates the EV hole in the tax base, and raises enough revenue to match highway outlays.

Immediately introducing a VMT tax for all vehicles may be administratively or politically difficult. The next best option to a full VMT tax is a VMT tax for commercial truck traffic paired with incremental changes to passenger car taxation.

Option 2 proposes the same VMT tax for commercial trucks as Option 1, fully replacing existing truck taxes, including the tax on diesel fuel. It would also introduce a $100 annual fee for passenger electric vehicles and raise the gas tax from 18.4 cents to 20.4 cents per gallon. The commercial VMT tax, the EV fee, and the gas tax would be inflation-indexed.

This hybrid approach achieves nearly all the objectives of the full VMT tax. Its main limitation is that a flat EV fee does not vary with miles driven, so low-mileage EV drivers would overpay and high-mileage EV drivers would underpay.

Option 2 has similar revenue effects as the full VMT tax. It would raise more than $250 billion for the HTF over the next decade and reduce overall deficits by $190 billion. Revenue would grow slightly more slowly than the full VMT tax, but the revenue raised would still be sufficient to eliminate the HTF shortfall in 2035.

Table 3. 10-Year Conventional Revenue from Replacing Truck Excise and Diesel Tax with VMT-Based Tax, Raising Gas Tax to 20.4 Cents, Introducing $100 Registration Fee for EVs, All Indexed for Inflation

Source: Authors’ calculations; EIA Annual Energy Outlook 2025, “Table 41. Light-Duty Vehicle Miles Traveled by Technology Type” and “Table 49. Freight Transportation Energy Use”; Bureau of Transportation Statistics, “Annual Vehicle Distance Traveled in Miles and Related Data by Highway Category and Vehicle Type: 2023”; Oregon Department of Transportation, “Mileage Tax Rates Effective Jan. 1, 2022”; Environmental Protection Agency, “Average Annual Vehicle Miles Traveled by Major Vehicle Category”; Congressional Budget Office, “The Budget and Economic Outlook: 2025 to 2035”; Tax Foundation General Equilibrium Model.

Option 3: Raise the Fuel Taxes

Option 3 would raise the existing gas and diesel tax rates to close the HTF funding gap. Raising the gas tax from 18.4 cents to 28 cents per gallon and raising the diesel tax from 24.4 cents to 40 cents per gallon would generate enough revenue to cover highway outlays in 2026. Both rates would be inflation-indexed.

Raising existing taxes would require no new administrative or compliance initiatives. However, continued reliance on the gas tax leaves freight underpriced and the EV gap in the tax base unresolved. That undermines the goal of neutral treatment across vehicle types and means the policy is not future-proof. As EV adoption continues, the gap will widen and the deficit will reemerge.

Option 3 would generate $188 billion for the HTF over the next decade and reduce overall deficits by $143 billion. The amount of additional revenue collected actually declines later in the 10-year budget window, despite inflation adjustments, because the tax base is projected to shrink. While revenue would exceed highway outlays in 2026 under this option, the deficit would end up returning in 2028 and would rise to over $15 billion by 2035, almost the same deficit the HTF faces today.

Table 4. 10-Year Conventional Revenue Estimate for Raising Gas and Diesel Taxes

Source: Authors’ calculations; Congressional Budget Office, “The Budget and Economic Outlook: 2025 to 2035,” Jan. 17, 2025, https://www.cbo.gov/publication/60870; Tax Foundation General Equilibrium Model.

Option 4: Flat Registration Fees

Option 4 would replace all existing HTF taxes with annual registration fees that vary by gross vehicle weight rating.

This is a radical reform option with several advantages. Flat annual registration fees would be simpler than the current mix of HTF taxes and be insulated from the shift toward EVs, providing a stable source of revenue.

However, it has some obvious problems too. While all drivers would contribute to road maintenance, the fee would not vary by mileage—someone who drives 5,000 miles a year would pay the same fee as someone who drives 25,000 miles. Without accounting for miles driven, a flat registration fee would be a weaker user feeA user fee is a charge imposed by the government for the primary purpose of covering the cost of providing a service, directly raising funds from the people who benefit from the particular public good or service being provided. A user fee is not a tax, though some taxes may be labeled as user fees or closely resemble them. model than the gas tax, at least for non-EVs.

Option 4 would generate $237 billion for the HTF over the next decade and reduce overall deficits by $181 billion. Revenue nearly matches highway outlays even in year 10, and it continues to grow as the vehicle stock expands, particularly among commercial vehicles.

Table 5. 10-Year Conventional Revenue Estimate for Flat Registration Fees Replacing All Highway Trust Fund Revenue

Source: Authors’ calculations; EIA Annual Energy Outlook 2025, “Table 39. Light-Duty Vehicle Stock by Technology Type” and “Table 49. Freight Transportation Energy Use”; Bureau of Transportation Statistics, “Annual Vehicle Distance Traveled in Miles and Related Data by Highway Category and Vehicle Type: 2023”; Environmental Protection Agency, “Average Annual Vehicle Miles Traveled by Major Vehicle Category”; Congressional Budget Office, “The Budget and Economic Outlook: 2025 to 2035”; Tax Foundation General Equilibrium Model.

A full schedule of registration fees appears in the appendix. To generate revenue estimates, we used average weights for different classes of vehicles. The average passenger car rate of $118.84 applies to vehicles with GVWRs between 4,000 and 6,000 pounds. The average commercial truck rate of $2,079.73 applies to trucks with GVWRs between 44,000 pounds and 46,000 pounds. We assume 1 percent of the vehicle stock for both trucks and passenger vehicles is part of public sector fleets.

Table 6. Revenue Collected by Registration Fees per Category, 2026

Source: Authors’ calculations; EIA Annual Energy Outlook 2025, “Table 39. Light-Duty Vehicle Stock by Technology Type” and “Table 49. Freight Transportation Energy Use”; Bureau of Transportation Statistics, “Annual Vehicle Distance Traveled in Miles and Related Data by Highway Category and Vehicle Type: 2023”; Environmental Protection Agency, “Average Annual Vehicle Miles Traveled by Major Vehicle Category”; Congressional Budget Office, “The Budget and Economic Outlook: 2025 to 2035”; Tax Foundation General Equilibrium Model.

How Do These Options Change the Highway Trust Fund’s Fiscal Picture?

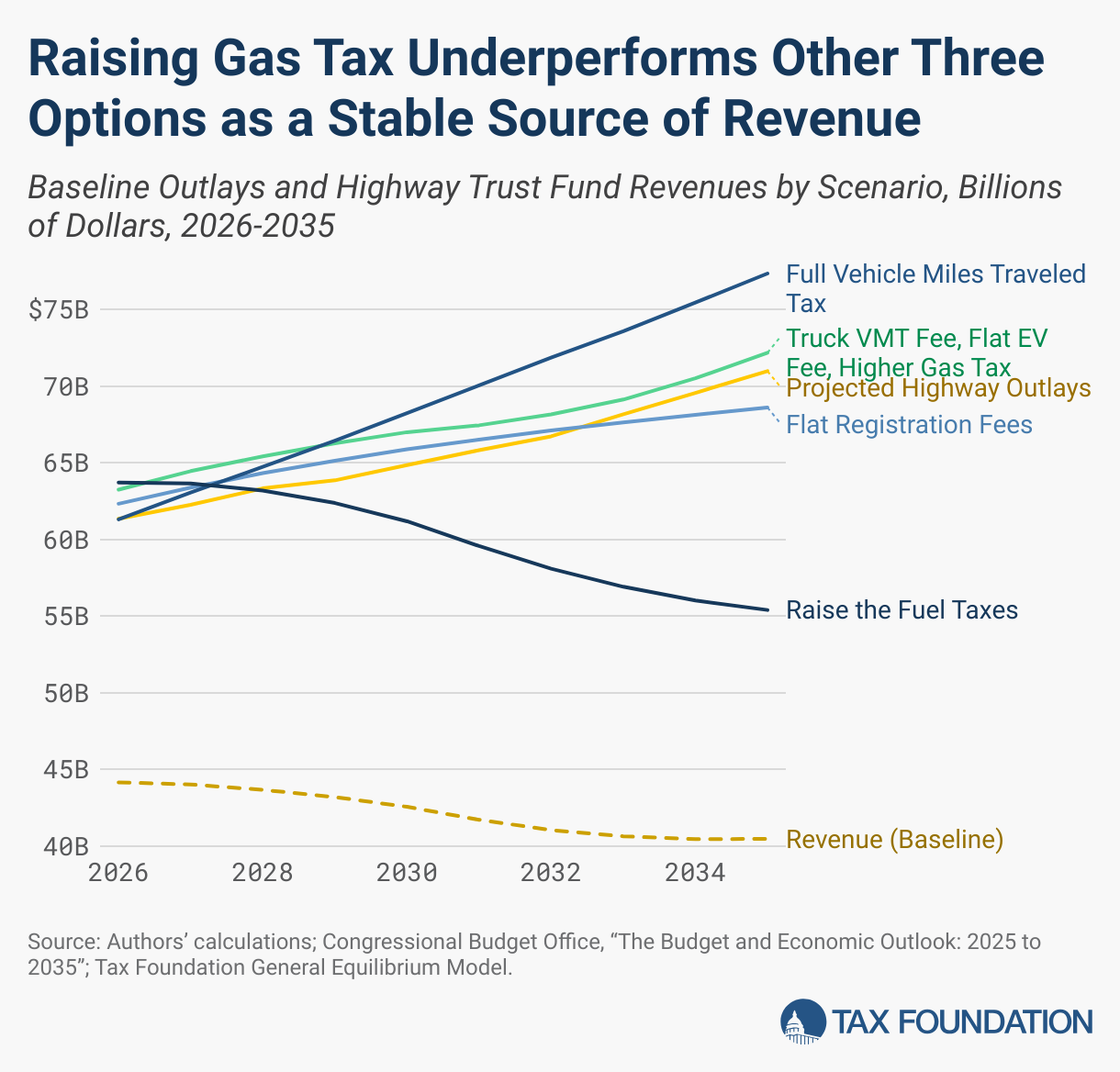

Taken together, the four options illustrate how different approaches to highway funding would—or would not—provide a long-term fiscal solution to the HTF’s shortfall.

Examining total HTF revenue per year under each option, rather than focusing on the change in revenues flowing into the trust fund or the conventional revenue estimate, provides a clearer picture of each option’s relative effectiveness.

The chart below compares projected highway outlays, projected highway revenues, and total highway revenues under the four options. Options 1, 2, and 4 all outperform the fuel tax increase (Option 3). All four options raise enough revenue to match highway outlays in 2026, but the deficit reappears very quickly under Option 3, whereas the other options continue to roughly match spending throughout the 10-year budget window.

That said, raising the gas and diesel taxes would still leave the HTF in a stronger position than another reauthorization that relies on general fund transfers.

Partial Options

Each option we modeled offers a way to match highway spending to highway revenue, at least in 2026. The strongest option is the full VMT tax, but Option 2 (the combination of the truck-based VMT tax, a higher gas tax, and EV registration fees) comes close. The other options are less structurally sound but still provide short-term fiscal solutions.

Short of closing the gap entirely, other reforms could improve the trust fund’s fiscal situation and shift more costs toward users.

For example, in May 2025, the initial House version of the One Big Beautiful Bill Act included new registration fees for all passenger vehicles: $20 per year for internal combustion engine (ICE) vehicles, $100 for hybrids, and $200 for EVs. The Transportation and Infrastructure Committee’s markup draft eliminated the ICE vehicle fee but increased the EV registration fee to $250.

We estimated the final House version would raise $78 billion from 2026 through 2035 for the HTF, and reduce the overall budget deficit by $58 billion.[17] The policy was later removed in the Senate.[18]

Another proposal from 2025, the Fair SHARE Act, would impose a one-time $1,000 fee on EVs and a $550 fee on battery modules over 1,000 pounds. We estimated it would raise $49 billion in revenue for the HTF over 10 years, and reduce the overall budget deficit by $36 billion.[19]

Both proposals would help the HTF, but they would not solve its long-term imbalance.

Implementation Issues: Feasibility, Privacy, and Equity

Three major considerations shape the design of any VMT tax:

- Administrative feasibility: How well could the government track vehicle miles traveled and assess liability?

- Privacy: Would mileage tracking infringe on civil liberties?

- Equity: Would a VMT tax fall unevenly on certain populations?

Feasibility and Privacy

Administrative feasibility and privacy often conflict. Several approaches could support mileage reporting, ranging from high-tech devices to low-tech manual submissions.

The most precise option would use GPS tracking, which can record miles traveled and allocate them among jurisdictions while exempting private roads. But GPS tracking raises serious privacy concerns.

To mitigate privacy concerns, several state-level VMT tax programs have used third-party private-sector commercial account managers (CAMs). CAMs strip out nonessential data before transmitting aggregate miles traveled to tax authorities. Though it protects privacy, concerns about data storage, security, and accessibility remain.

Newer vehicles with advanced telematics could use software or hardware to record mileage by jurisdiction while keeping location data private. Similar devices are already popular in insurance markets, monitoring vehicle usage and discounting insurance for people who drive less or more safely.[20] This reporting method would not be able to automatically exempt private roads or differentiate between states, but it would protect drivers’ location data.

The lowest-tech solution would involve manually submitting odometer readings or photographs to report miles traveled. This minimizes intrusion but increases administrative and compliance costs.

At the federal level, tracking and privacy risks can be minimized. Unlike states, a federal VMT tax only requires knowing the total number of miles driven, not the location. Miles driven on private or foreign roads would need exemptions, which could be handled through manual submissions or a standard deductionThe standard deduction reduces a taxpayer’s taxable income by a set amount determined by the government. Taxpayers who take the standard deduction cannot also itemize their deductions; it serves as an alternative. for exempt miles driven. Drivers with higher miles on private roads could submit specific claims to prevent overcharging, but most of the compliance and administrative costs could be avoided with a standard deduction for private roads and out-of-country driving.[21]

If the federal VMT infrastructure is used for state-level programs, more detailed tracking may be required. In that case, a third-party reporting system could allocate miles driven across jurisdictions without recording specific locations or timestamps.

Administrative Costs

Another feasibility question is how affordably such a tax could be administered. One advantage of the existing gas tax is its relatively low administrative and compliance costs because it is collected upstream from a small number of taxpayers.[22] A system where each driver becomes a taxpayer would potentially increase costs.

For a freight VMT fee, Oregon demonstrates that efficient administration is possible, relying on a combination of self-reported odometer readings and automated device data collections. The CBO estimates Oregon’s administrative costs are around $20 per truck per year.[23]

Given that a typical heavy commercial truck traveling more than 50,000 miles per year would owe more than $5,000 under our proposed VMT-based taxes in Options 1 and 2, Oregon’s experience suggests the administrative costs would be low relative to the revenue raised for freight taxpayers. Federal implementation could be even more efficient, especially because many fleets already use electronic logging devices.

Administrative costs of $10 to $20 per year per taxpayer are insignificant for freight taxpayers, but may be more meaningful for passenger-vehicle owners, whose annual tax would likely fall between $100 and $200. Automatic payment systems or smartphone apps could further reduce administrative and compliance costs, but the difference reinforces the case for a freight-first rollout.

Equity Considerations

Equity is another major concern for transportation taxes, especially regarding income and urban-rural differences.

The existing gas tax functions as a proxy user fee but introduces disparities because of differences in fuel efficiencies. Higher-income drivers tend to own newer, more fuel-efficient vehicles, paying less per mile of road use. Lower-income drivers, who are more likely to own older, less efficient vehicles, pay more relative to the road wear they cause. The rapid rise of electric vehicles exacerbates the imbalance, as EVs avoid the gas tax entirely.

Similarly, rural drivers often face higher tax burdens because they tend to drive longer distances and less efficient vehicles. Although heavier rural vehicles cause somewhat more road wear, this only partially offsets the disparity.

A VMT tax, particularly one that accounts for vehicle weight, would better align charges with road use and infrastructure costs. By tying tax liability to miles driven and damage caused, a VMT tax would reduce regressivity and the urban-rural disparity, restoring the user-pays principle to roads. Empirical analysis from the Eastern Transportation Coalition’s Phase 5 Report supports these findings with studies across six states.[24]

While a VMT tax would still affect groups differently—rural drivers generally drive further than urban drivers and thus would pay more—it would be fairer overall than the gas tax. Differentiating rates by road type (for example, discounting miles traveled on less costly rural roads) could further enhance fairness, though it would require more sophisticated data collection and raise additional privacy concerns.

A VMT tax would still be regressive, but it represents a more neutral, equitable, and efficient user fee than the current gas tax, which disproportionately benefits wealthier, urban, and EV drivers.

Conclusion

A VMT tax is the most efficient and sustainable option for US highway funding amid rapidly changing markets and technologies. It best achieves the user-pays principle, aligning taxes paid with actual road use, vehicle weight, and infrastructure costs.

That said, a full VMT system would be complex to establish and administer. A hybrid approach, replacing truck-related excise taxes with a VMT tax on freight, retaining the gas tax, and adding flat registration fees on passenger traffic, delivers most of the same benefits with fewer administrative challenges.

Fixing the HTF will require legislative and administrative effort. But an efficient, privacy-conscious, and equitable solution is achievable now.

With the next highway bill, lawmakers have the opportunity to embrace economic efficiency and fiscal responsibility by returning to the user-pays principle that has long underpinned America’s transportation infrastructure.

Note: To acess the full report, including the Appendix, click the “Download PDF” button at the top of the page.

[1] U.S. Department of Transportation, “Advancing a Surface Transportation Proposal That Focuses on America’s Most Fundamental Infrastructure Needs,” Federal Register, Jul. 21, 2025, https://www.federalregister.gov/documents/2025/07/21/2025-13663/advancing-a-surface-transportation-proposal-that-focuses-on-americas-most-fundamental-infrastructure.

[2] 0.1 cents per gallon of each fuel tax is allocated to the Leaking Underground Storage Tank (LUST) Trust Fund.

[3] Congressional Budget Office, “Baseline Projections: Highway Trust Fund Accounts,” January 2025, https://www.cbo.gov/system/files/2025-01/51300-2025-01-highwaytrustfund.pdf.

[4] H.R.3684 – Infrastructure Investment and Jobs Act, https://www.congress.gov/bill/117th-congress/house-bill/3684.

[5] Alex Muresianu, Adam Hoffer, Jacob Macumber-Rosin, and Alex Durante, “Expanding User Fees for Transportation: Roads and Beyond,” Tax Foundation, Aug. 7, 2024, https://taxfoundation.org/research/all/federal/vehicle-miles-traveled-vmt-tax-transportation/.

[6] Ibid. See also Alex Muresianu and Adam Hoffer, “EVs and the Highway Trust Fund: Five Things to Know,” Tax Foundation, Mar. 4, 2025, https://taxfoundation.org/blog/ev-highway-trust-fund/.

[7] Michael Gorman, “A Vehicle Mileage Tax for Heavy Trucks?” Regulation (Winter 2024-2025), https://www.cato.org/sites/cato.org/files/2024-12/regulation-v47n4-3.pdf.

[8] Michael Gorman, “The Economic Costs of Public Subsidies for Freight Transportation,” Information Technology and Innovation Foundation, Sep. 8, 2025, https://itif.org/publications/2025/09/08/the-economic-costs-of-public-subsidies-for-freight-transportation/.

[9] Congressional Budget Office, “10-Year Budget Projections,” January 2025, https://www.cbo.gov/data/budget-economic-data.

[10] William McBride, Erica York, Alex Durante, and Garrett Watson, “The Unsustainable US Debt Course and Impacts of Potential Tax Changes,” Tax Foundation, Jan. 14, 2025, https://taxfoundation.org/research/all/federal/us-debt-budget-taxes-spending-social-security-medicare/.

[11] Allan Bradley and Papa-Masseck Thiam, “Analysis of Car and Truck Pavement Impacts,” FP Innovations, October 2018, https://www.trucking.org/sites/default/files/2022-01/Analysis%20of%20car%20and%20truck%20pavement%20impacts-FINAL.pdf.

[12] Oregon Department of Transportation, “Mileage Tax Rates,” https://www.oregon.gov/odot/Forms/Motcarr/9928-2022.pdf.

[13] Vasili Varlamos, “Two Oregon Senate Democrats Urge Kotek to Sign Transportation Bill ‘Without Further Delay,’” KATU 2 ABC, Oct. 27, 2025, https://katu.com/news/politics/two-oregon-senate-democrats-urge-kotek-to-sign-transportation-bill-without-further-delay-salem-portland-politics-taxes-voters-referendum-republicans.

[14] Huaqun Li, Garrett Watson, and Erica York, “Overview of the Tax Foundation’s General Equilibrium Model,” Tax Foundation, Mar. 5, 2025, https://taxfoundation.org/research/all/federal/general-equilibrium-model/.

[15] Michael Gorman, “A Vehicle Mileage Tax for Heavy Trucks?” Regulation (Winter 2024-2025), https://www.cato.org/sites/cato.org/files/2024-12/regulation-v47n4-3.pdf.

[16] Ibid.

[17] Alex Muresianu, “Fixing Highway Funding in the Reconciliation Package,” Tax Foundation, May 27, 2025, https://taxfoundation.org/blog/ev-tax-credit-reconciliation-bill-highway-funding/.

[18] Andres Picon, “The EV and Hybrid Fee is Dead—For Now,” E&E News, Jun. 17, 2025, https://www.eenews.net/articles/the-ev-and-hybrid-fee-is-dead-for-now/.

[19] Alex Muresianu and Adam Hoffer, “EVs and the Highway Trust Fund: Five Things to Know.”

[20] See Daniel Robinson, “Progressive Snapshot,” Marketwatch Guides, Dec. 26, 2023, https://www.marketwatch.com/guides/insurance-services/progressive-snapshot/; Daniel Robinson, “State Farm Drive Safe and Save,” Marketwatch Guides, Jun. 22, 2024, https://www.marketwatch.com/guides/insurance-services/state-farm-drive-safe-and-save/.

[21] Washington State Transportation Commission, “Forward Drive: Sustaining Washington State’s Transportation System Into the Future,” January 2024, https://waroadusagecharge.org/media/final-report/DIGITAL_WA%20RUC%20Final%20Report%20January%202024_v2.pdf.

[22] See, for instance, Shuting Pomerleau, “Administrative Costs of a Carbon TaxA carbon tax is levied on the carbon content of fossil fuels. The term can also refer to taxing other types of greenhouse gas emissions, such as methane. A carbon tax puts a price on those emissions to encourage consumers, businesses, and governments to produce less of them.,” Niskanen Center, February 2021, https://www.niskanencenter.org/wp-content/uploads/2021/02/Jan28-Administrative-Costs-of-Carbon-Tax.pdf.

[23] Perry Beider and David Austin, “Issues and Options for a Tax on Vehicle Miles Traveled by Commercial Trucks,” Congressional Budget Office, October 2019, https://www.cbo.gov/system/files/2019-10/55688-CBO-VMT-Tax.pdf.

[24] The Eastern Transportation Coalition, “Phase 5 STSFA Grant Report,” Fall 2025, https://tetcoalitionmbuf.org/wp-content/uploads/2025/09/TETC-P5-Final-Report_9-17-2025_508.pdf.

Share this article